Introduction

According to a recent report, over $4.1 billion was lost to DeFi hacks in 2024. As cryptocurrencies gain traction and gain more users, the topic of tax implications for digital assets remains a significant concern. In this article, we will delve into Coinbase crypto tax deduction strategies that can help you optimize your returns while staying compliant with regulations. Let’s break it down.

Understanding Crypto Taxes

First, let’s establish the fundamental concepts. In Vietnam, the growing number of cryptocurrency investors, with an estimated growth rate of 25% in 2023, has necessitated a clear understanding of crypto tax regulations, or tiêu chuẩn an ninh blockchain. Cryptocurrencies, like Bitcoin and Ethereum, are taxed as property rather than currency. This means that when you sell, trade, or use your crypto for purchases, it may trigger a taxable event.

Key Tax Implications

- Capital Gains Tax: If your crypto assets appreciate in value, you’ll owe taxes on that increase when you sell them.

- Short-term vs. Long-term: Gains on assets held for less than a year are taxed at your ordinary income rate, while those held longer benefit from lower capital gains rates.

- Losses: You can offset your capital gains with losses, a strategy known as tax-loss harvesting.

Coinbase Tax Documentation

Coinbase provides tools to help manage your crypto tax responsibilities effectively. They generate tax documents that can help simplify your filing process.

Using Coinbase Reports

Coinbase users can access tax documents directly from their accounts. Here’s how:

- Log in to your Coinbase account.

- Navigate to the Reports section.

- Download your transaction history for the tax year.

This report will typically include details regarding sales, exchanges, and other transactions, which are crucial for preparing your tax returns.

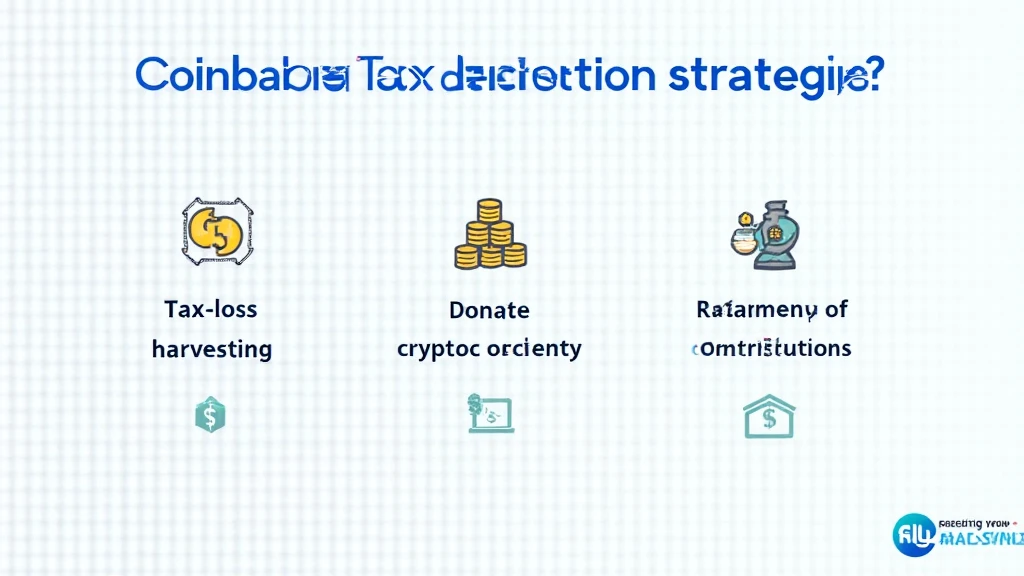

Strategies for Deductions

While taxes on cryptocurrency can be burdensome, strategic planning can help minimize your liabilities. Here are some effective Coinbase crypto tax deduction strategies.

1. Tax-Loss Harvesting

Tax-loss harvesting involves selling assets that have decreased in value to offset taxes on gains from other investments. This can be particularly effective during market downturns.

2. Donating Cryptocurrency

You can receive a tax deduction for donating appreciated cryptocurrency to eligible charities. This can be a win-win, as you won’t have to realize capital gains.

3. Contributing to a 401(k)

If you hold Bitcoin or other cryptocurrencies in a retirement account, such as a self-directed 401(k), you can delay taxes on those holdings until you withdraw them in retirement, potentially reducing your overall taxable income during your earning years.

Impact of Regulations in Vietnam

The Vietnamese government has begun addressing the regulatory framework for cryptocurrencies, including the requirement for businesses conducting crypto transactions to register with the government. The effects of these regulations on tax obligations and crypto operations are critical for investors.

Analyzing Local Regulations

Compliance is increasingly important as regulations evolve. Here’s what to keep an eye on:

- Registration: Businesses dealing in cryptocurrencies must be registered, providing tax information to the government.

- Tax Compliance: Ensure all taxes related to cryptocurrency transactions are filed accurately to avoid penalties.

Record-Keeping Best Practices

To substantiate your tax claims, maintaining thorough records of all transactions is vital. Here are some tips:

- Document the date, amount, and purpose of each transaction.

- Keep track of exchange rates and fees where applicable.

- Utilize tax software that integrates with Coinbase for easier expense tracking.

Conclusion

In conclusion, navigating cryptocurrency tax obligations can be daunting, but employing the right Coinbase crypto tax deduction strategies can enhance your financial outcomes while ensuring compliance. Remember, the landscape is evolving, so stay informed about any changes in both global and local Vietnamese regulations related to cryptocurrencies. For expert advice, consider consulting a tax professional who understands the complexities involved in reporting crypto assets.

As always, it’s beneficial to take proactive measures in understanding your tax obligations and seeking strategies to optimize your returns effectively. To learn more about cryptocurrency and taxation in Vietnam, check out our link on hibt.com.

About the Author: Dr. Nguyen An, a blockchain technology expert and tax compliance consultant, has authored over 15 papers in the field and led audits on prominent crypto projects addressing the rapidly evolving landscape.